Minister of Housing, Infrastructure and Communities Transition Binder (2025)

Book 5: State of Housing, Homelessness and Infrastructure in Canada

- Section A: State of Housing and Homelessness

- Housing challenges are multifaceted and complex

- Domestic trends impact the supply and demand for housing

- Barriers to increasing housing supply are wide ranging

- Affordability challenges extend beyond homeowners as renters face significant pressures

- Housing needs are uneven – different regions and rural and northern communities have distinct and often greater needs

- The current crisis is exacerbating acute homelessness challenges

- Multi-jurisdictional responsibilities and varied ownership mean other levels of government, the private sector, and non-profits have key roles to play

- The federal government has taken a leadership role in addressing housing and homelessness challenges

- Section B: State of Infrastructure

- Does Canada have the right kind of infrastructure to meet current and future needs?

- What is infrastructure?

- HICC Program Contribution Decisions Since 2016

- Infrastructure as a shared priority

- Infrastructure investments have almost doubled in the last two decades

- Understanding Infrastructure average age and remaining service life helps asset owners to inform early planning and management

- The condition of infrastructure in Canada

- Asset management capacity is lower in smaller municipalities, and varies significantly among provinces and territories

- Current and future infrastructure investments are influenced by key economic, socio-demographic and environmental factors

- Cross-sectoral impacts of infrastructure - The economy

- Beyond construction's immediate impact, infrastructure investment contributes to long-term economic competitiveness

- A highly productive construction sector is critical to growing our infrastructure

- Declining construction sector productivity risks limiting our ability to deliver Canada's infrastructure needs

- The construction sector is home to high paying jobs but the benefits are not equal across different working groups

- Construction materials are an integral part of infrastructure delivery and subject to volatility

- Cross-sectoral impacts of infrastructure - The environment

- Infrastructure is crucial to mitigating and adapting to climate change

- Infrastructure is highly impacted by climate change

- Resilient infrastructure requires efficient designs and planning

- Environmental improvements are being made during the construction of infrastructure assets

- Cross-sectoral impacts of infrastructure - Our communities

- The state of infrastructure – A summary

- Section C: State of Transit

- Does Canada have the right kind of transit infrastructure to meet current and future needs?

- Why is it important to invest in public transit and what is HICC's role?

- The Canada Public Transit Fund provides permanent funding to address a range of transit needs

- Current stock, investment and condition of transit infrastructure

- Current Outcomes

- Future infrastructure needs

- The state of transit – summary

- Annex: Regional Lens

Section A: State of Housing and Homelessness

Housing challenges are multifaceted and complex

Canada is facing a housing crisis

- Middle-income households across the country are finding it increasingly hard to buy homes. These households are often staying in rental housing longer, placing additional pressures on rental supply and increasing rental costs.

- Lack of affordable housing means Canadians find it harder and harder to secure housing where they work or move for jobs, hurting economic growth.

- Vulnerable populations and lower-income households are struggling to have their basic housing needs met due to a lack of suitable affordable housing.

- Rising homelessness and unsheltered homelessness is driven by housing system gaps related to non-market (including transitional and supportive housing), exacerbated by systemic failures along with individual circumstances.

Key challenges in the housing system

Affordability

A crisis that impacts both low-income and middle-class Canadians.

Stability

Canada’s financial system at greater risk from rising house prices and debt.

Sustainability

Need to shift new and existing housing to climate compatibility.

Productivity

Need to improve technology adoption and address labour shortages.

Governance

Canada’s growing and changing population requires a coordinated housing strategy.

Reconciliation/Equity

Entrenched, systematic barriers prevent access to affordable housing.

-

Figure 1 - Text version

Canada’s Supply Gaps, by province (2023) Province Current projection of 2030 housing stock Incremental housing units required to meet demand Ontario 6,610,000 1,480,000 Quebec 4,450,000 860,000 British Columbia 2,580,000 610,000 Alberta 2,090,000 130,000 Manitoba 650,000 170,000 Saskatchewan 550,000 60,000 Nova Scotia 510,000 70,000 New Brunswick 390,000 0 Newfoundland and Labrador 270,000 60,000 Prince Edward Island 80,000 0

Sources: based on CMHC data (2023)

Domestic trends impact the supply and demand for housing

High population growth

High population growth largely via newcomers mostly settling in urban areas means that Canada leads G7 countries by far in population growth; rapid population growth has been compounding pressures and costs for communities.

-

Figure 2 - Text version

Contribution to annual population change 2001-2022 Year Non-Permanent Residents Permanent Residents Births Minus Deaths Other 2001 33,510 204,425 108,284 -7,875 2003 10,348 183,798 110,095 -7,895 2005 15,978 200,122 123,247 -10,886 2007 51,478 198,525 140,296 -31,887 2009 34,243 228,561 144,829 -31,800 2011 55,400 205,157 137,666 -24,049 2013 32,867 214,435 129,755 -23,983 2015 35,448 268,291 122,022 -19,456 2017 33,510 204,425 108,284 8,244 2019 75,265 252,484 74,126 8,268 2021 208,689 445,983 41,398 0 2022 697,701 433,480 27,524 0

Sources: StatCan Table 17-10-0151-01

Labour shortages

Labour shortages challenge the construction sector; aging workforce with fewer young people pursuing trades means growing gaps between predicted needs and growth. Opportunities to align future skills and needs in new industries (e.g., modular, pre-fab).

-

Figure 3 - Text version

Predicted Growth in the Labour Force vs. Predicted Growth Required to Keep up with Investment 2023-2032 Year Predicted Growth (Thousands) Predicted Required Growth (Thousands) 2023 53618.7 40766.5 2024 57470.7 41713.4 2025 57532.5 42503.9 2026 56857.7 41724.4 2027 56687.5 42068.9 2028 58932.4 42359.3 2029 59181.4 42598.5 2030 57660.6 42791.5 2031 59774.6 42949.2 2032 60085.9 43071.2 Note: Required growth based on estimates of retirements and a 2.8% average annual growth in real investment.

Source: Economic Analysis and Modelling, HICC

Increasing home unaffordability impacts ability to access and maintain housing

In 2023, home ownership costs rose to 62.5% of household income while average rent growth reached a record high 8%, exceeding both inflation (4.7%) and wage growth (5%).

-

Figure 4 - Text version

Ownership Costs as % of Household Income, Canada Year Ownership Costs as % of Household Income (Historical until 2020, Forecast for 2025) Q1 1985 41.9% Q2 1985 39.8% Q3 1985 38.8% Q4 1985 38.6% Q1 1990 50.8% Q2 1990 56.6% Q3 1990 53% Q4 1990 50.4% Q1 1995 43.8% Q2 1995 39.6% Q3 1995 38.9% Q4 1995 38.3% Q1 2000 37% Q2 2000 37% Q3 2000 36.6% Q4 2000 36.2% Q1 2005 36.5% Q2 2005 36.6% Q3 2005 36.7% Q4 2005 38.2% Q1 2010 39.5% Q2 2010 41.7% Q3 2010 40.8% Q4 2010 39.7% Q1 2015 38.2% Q2 2015 37.8% Q3 2015 38.2% Q4 2015 39% Q1 2020 42.2% Q2 2020 41.5% Q3 2020 41.2% Q4 2020 41.4% Q1 2025 54.5% Q2 2025 52.3% Q3 2025 51.9% Q4 2025 51.3%

Sources: RBC Thought Leadership (2023)

Barriers to increasing housing supply are wide ranging

Increasing costs

The cost to construct a residential building in Canada has increased by 58% since 2020, well outpacing overall inflation rate; tariffs could increase costs further.

Restrictive and time-consuming planning processes

Zoning laws and planning restrictions limit the construction of high-density housing near infrastructure and transit.

Inconsistent government investment

Reduced investments in housing over decades have left gaps in affordable and supportive housing.

(Still) High Interest Rates

Higher interest rates have slowed the economy and reduced the pace of home construction.

Low productivity

The Canadian construction sector lags its counterparts with low rate of adoption of new technologies.

-

Figure 5 - Text version

Construction Sector Productivity Year All Industries (Average) Construction [BS23] Residential building construction [BS23A] 2000 52.3 51.4 45.8 2001 53.1 53.6 48.1 2002 54 54.8 48.8 2003 54.2 55.8 48.7 2004 54.8 55.3 47.2 2005 56 55 46.7 2006 56.8 54.2 45.2 2007 56.9 53.6 45.2 2008 56.6 51.3 43.2 2009 56.6 52.1 46.1 2010 57.2 52.3 46.7 2011 58.2 52.7 47.9 2012 58.3 52.7 46.2 2013 59.2 54 48 2014 61 54.7 49.5 2015 61 53.7 51.3 2016 61.3 54 52.9 2017 62.2 53.8 51.5 2018 62.5 54.2 52.2 2019 62.7 53.4 51.1 2020 67.7 59.9 59.9 2021 65 54.2 51.4 2022 64.6 52.5 47.4 2023 63.5 48.7 42.1

Source: StatCan Table 36-10-0480-01

-

Figure 6 - Text version

Estimated Average Permitting Timelines by Municipality Municipality Average Approval Times (Months) Charlottetown 3 Saskatoon 4 Winnipeg 5 Calgary 5 Edmonton 7 St. John’s 8 Ottawa 13 Vancouver 15 Halifax 21 Toronto 32

Sources: Canadian Home Builders’ Association’s (CHBA’s) Municipal Benchmarking Study (2022)

Municipalities have identified barriers to accelerating residential permitting timelines

- Quality of submissions vary, and low-quality submissions require additional municipal time and resources; resubmissions can take a long time.

- Some municipalities work with applicants for longer periods of time, which could be more conducive to getting more built in the long run.

Certain permitting practices can help municipalities build more, faster

- Use of online portals.

- Issuing conditional building permits, allowing construction to begin.

- Evaluating/triaging projects according to risk categories & housing design catalogue.

- Encouraging higher-density applications; may take less time on a per-unit basis.

Affordability challenges extend beyond homeowners as renters face significant pressures

Demand for rental housing continues to be strong with low rental vacancy in 2024 (2.2%) driven by growing population, combined with years of under supply and increasing cost of homeownership.

Canada’s housing system has become financialized in recent decades, with real estate seen as an investment asset:

- Early estimates from the Federal Housing Advocate suggest 20 to 30% of Canada’s purpose-built rental housing is owned by institutional investors.

High rent increases upon turnover of units signal market imbalance:

- The change in average rents in 2-bedroom turnover units far exceeded the change in rents in non-turnover 2-bedroom units in 2024 (23.5% vs. 3.5%).

- Cities in provinces with rent control had lower turnover rates than cities in provinces with rent control which led to higher average turnover rent increases.

As a result of low public investments since the 1990s, non-market housing makes up a small proportion of the housing system (approximately 4%) – affordable units are being lost due to age, disrepair, or conversion to market rents.

Lack of growth in purpose-built affordable rental housing combined with the diminishing non-market housing stock is impacting social areas beyond housing (e.g., health) and disproportionately affecting newcomers, vulnerable and lower-income groups.

| Overall change in average Rent (2-bed) | Turnover unit average rent change when turned over (2-bed) | Provincial rent guideline indicator | |

|---|---|---|---|

| Canada | 5.40% | 23.50% | N/A |

| Vancouver | 5.50% | 26.50% | Yes |

| Edmonton | 7.00% | 10.90% | No |

| Calgary | 8.90% | 18.70% | No |

| Toronto | 2.70% | 40.70% | Yes |

| Ottawa | 5.00% | 23.80% | Yes |

| Montréal | 6.30% | 18.70% | Yes |

| Halifax | 3.80% | 28.30% | Yes |

Sources: CMHC Fall Rental Market Report (2024).

-

Figure 8 - Text version

% of social rental Country or Region % of Social Rental Dwellings Netherlands (NL) 34.06838 Denmark (DK) 21.33333 United Kingdom (UK) 16.36392 France (FR) 14.00771 Ireland (IE) 12.69586 Finland (FI) 10.93878 Switzerland (CH) 3.617056 Poland (PL) 6.645129 Australia (AU) 3.227404 Norway (NO) 4.1024 Italy (IT) 2.402509 United States (US) 3.6209 Canada (CA) 3.472193 Japan (JP) 3.079622 Germany (DE) 2.55664 Portugal (PT) 1.058791 Spain (ES) 1.070074 Columbia (CO) 0.00643 Note: Canada non-market housing share is well below the 7% OECD average.

Sources: Scotiabank Economics, OECD

Housing needs are uneven – different regions and rural and northern communities have distinct and often greater needs

Housing needs differ across regions

Housing needs differ across regions based on unique demographic, geographic, and economic realities.

- Relative climates and unique supply chains influence provincial building codes which have direct impact on materials used in local residential construction.

- The prevalence of extreme weather events differ across the country with wildfires more prevalent in western Canada, while heat domes and severe storms are projected to worsen in the east.

- There has been a growing mismatch between the housing types being built and those preferred and needed.

Rural and northern communities

Rural and northern communities are challenged to build housing and infrastructure with higher costs, lower revenues, and limited capacity.

- Those in the north also see a shorter construction season, higher transportation, material and labour costs, greater climate impacts and a high proportion of non-market housing.

- Smaller communities dependent on tourism and post-secondary institutions face important challenges for workforce housing as well as maintaining affordable and transparent rental options to accommodate population changes.

Homelessness, in rural and remote areas

Homelessness, including encampments, is increasingly being seen in rural and remote areas requiring different types of supports depending on their size and capacity to respond.

-

Figure 9 - Text version

Rate of Core Housing Need Province or Territory Rate of Core Housing Need (percentage) Alberta 11.3% British Columbia 16.0% Manitoba 12.0% New Brunswick 9.2% Newfoundland & Labrador 9.4% Nova Scotia 12.9% Northwest Territories 13.2% Nunavut 32.9% Ontario 14.5% Québec 5.5% Prince Edward Island 6.5% Saskatchewan 9.5% Yukon 13.1% Note: 2021 Census data included COVID-19-related supports, which would in turn impact the calculation of core housing need.

Sources: StatCan & CMHC - 2022 Canadian Housing Survey (provinces) and the 2021 Census (territories)

The current crisis is exacerbating acute homelessness challenges

At the extreme end of the housing spectrum are those experiencing or at risk of homelessness. The lack of affordable and non-market housing impedes efforts to prevent entries to and facilitate exits from homelessness.

Shelter use dropped in 2020, due to the pandemic (i.e. reduced capacity to allow for physical distancing), but has increased since then as economic pressures and international geopolitics (e.g., increases in asylum claimants) have increased demands on the homeless-serving sector.

The number of people who experience homelessness each night has increased.

- In shelters: Average nightly use dropped in 2020 then rose 43% by 2023.

The Point-in-time count in 2024 showed that 57,000 people in 60 communities across Canada were identified as experiencing homelessness.

- This included 34,226 people experiencing homelessness in shelters, 16,684 in unsheltered locations (of whom, 4,425 were in encampments), and 6,241 who were provisionally accommodated in transitional housing programs.

Many more people experience homelessness throughout the year. Over 118,000 people accessed the shelter system alone in 2023.

- Length of shelter stays is increasing, suggesting increasing barriers to exiting homelessness.

- Of this group 28% (an estimated 32,660 people) experienced chronic homelessness in 2023, up from 22% (just under 27,000 people) in 2016.

-

Figure 10 - Text version

Estimated nightly homelessness rates in shelters and unsheltered areas 2017 - 2024 Year Unsheltered homelessness (across 55 communities participating in past 3 PiT counts) Shelter uses per night (average from annual shelter data) 2017 - 14,000 2018 3,922 15,000 2019 - 14,440 2020 - 11,600 2021 - 13,170 2022 7,702 16,248 2023 - 16,627 2024 16,114 -

Note: 2024 shelter user data is not yet available. PiT data from 2024 is not yet publicly available.

The Housing Continuum - Text version

- Homelessness

- Emergency Shelter

- Transitional Housing

- Surportive Housing

- Community Housing

- Affordable Housing

- Market Housing

Multi-jurisdictional responsibilities and varied ownership mean other levels of government, the private sector, and non-profits have key roles to play

Housing challenges are often localized; collaboration and partnership between all orders of government, as well as with the private and non-profit sectors, is critical.

- Housing is a shared responsibility, with overlapping mandates between level of governments

- Majority of housing is privately owned (e.g., 97% of new housing investment was private in 2023); community housing is more prominent in the territories, especially Nunavut.

| Federal Government | Provinces and Territories | Local Governments |

|---|---|---|

|

|

|

There have been calls for stronger federal governance and coordination amongst all level of governments from key actors, including the National Housing Accord, the Federal Housing Advocate, the Auditor General of Canada, the National Housing Council and the Social Housing and Human Rights Coalition.

The federal government has taken a leadership role in addressing housing and homelessness challenges

In recent years, the Government has committed significant resources to meet Canada’s housing objectives, with types and levels of interventions increasing over time.

| Federal Lever | Examples of Initiatives |

|---|---|

Tax Policy (DoF) |

|

Financial Sector Policies (DoF) |

|

Immigration Policies (IRCC) |

|

P/T bilateral transfers (CMHC) |

|

P/T/M Transfers (with conditionality) (HICC/CMHC) |

|

Low-cost loans & contributions (CMHC) |

|

Federal lands (PSPC) |

|

National standards and tools |

|

Other programs supporting housing ecosystem (e.g., ISED, ESDC, etc) |

|

-

Figure 11 - Text version

Federal housing investment since 2008 Years Federal Housing Investments since 2008 Global Financial Crisis (billions of dollars) 2007-08 2.155 2008-09 2.207 2009-10 3.028 2010-11 2.963 2011-12 2.048 2012-13 2.086 2013-14 2.085 2014-15 2.053 2015-16 2.008 2016-17 3.061 2017-18 2.756 2018-19 2.460 2019-20 4.841 2020-21 6.768 2021-22 8.253 2022-23 8.262 2023-24 11.244 Note: Amounts for 2007-08 until 2022-23 are actuals, as available. Amount for 2023-24 is an estimate, and subject to change. Amounts are on a cash basis. Amounts include Canada Mortgage and Housing Corporation (CMHC) programming only, and do not include: homelessness programming; energy efficiency programs delivered through Natural Resources Canada; tax measures; cost-matching provided by provinces and territories, or investments that support distinctions-based Indigenous housing strategies.

Sources: Budget 2024

Section B: State of Infrastructure in Canada

Does Canada have the right kind of infrastructure to meet current and future needs?

To answer this question, it is important to understand Canada’s current state of infrastructure, which can be assessed in a number of ways:

- Stock: Accumulation of an inventory of tangible infrastructure assets over time.

- Investment: Infrastructure spending for the purposes of construction of tangible assets.

- Condition: Standardized scale used to define the current state of an infrastructure asset (i.e., very good, good, fair, poor, or very poor).

Given the changing nature of Canadian society – demographic change, the growth of cities, climate change – understanding current assets cannot tell us whether what we have is what we will need in future.

All asset owners and governments need to be considering how future challenges will impact their need for infrastructure. This can be achieved through asset management practices, and efforts like the National Infrastructure Assessment Endnote *, which is intended to provide a long-term perspective on Canada's infrastructure needs.

What is infrastructure?

Infrastructure is a set of tangible assets that support the production, delivery and consumption of goods and services by governments, organizations and individuals. Examples of these assets include schools and hospitals; roads, rails and ports; potable water and water treatment facilities; and cultural and recreational facilities.

Governments generally support public infrastructure, which is subset of total infrastructure and refers to assets that provide a service to the public, such as public transit, broadband connectivity, electricity and libraries.

The construction of infrastructure involves a broad range of industries – ranging from natural resources (e.g., mining) and manufacturing (e.g., cement), to engineering and construction.

HICC Program Contribution Decisions Since 2016

- Since 2016, HICC has approved 11,939 projects, totaling over $62B. 2021 marks the beginning of the Rapid Expansion Fund announcements.

- Since 2016, public transit projects represent nearly 46% of announced projects, largely due to significant contributions to large-scale transit systems.

- Since 2020, highway and road program contributions have declined significantly, while resilience and natural infrastructure contributions were last made in 2023.

- Since 2020, the largest growth in program contributions have been in public buildings which comprise sport, recreation, culture, administration, and tourism, with over $1B committed in 2024.

-

Figure 12 - Text version

HICC Program Contributions, by Announcement Data abd Standardized Category Year Driking or Waste Water Highways and Roads Intercity Transit Other Public Buildings Public Transit Resilience and Natural Infrastructure Billions, current dollars ($) 2016 0.953 1.095 0.0724 0.075 0.215 1.333 0.225 2017 1.268 1.750 0.091 0.499 0.294 3.825 0.058 2018 0.144 0.625 0.024 0.080 0.165 3.952 3.597 2019 0.451 2.085 0.039 0.589 0.544 3.308 0.357 2020 0.429 0.339 0.014 0.232 0.251 0.393 0.143 2021 0.744 0.215 0.005 1.508 1.278 6.834 1.712 2022 0.557 0.029 0.010 0.224 0.790 1.036 0.263 2023 0.224 0.183 0.042 0.472 0.751 2.271 1. 567 2024 0.233 0.123 0.006 0.409 1.096 0.736 - 2025 0.123 0.012 0.009 0.408 0.061 2.608 -

Source: HICC Infrastructure Funding Report

Infrastructure as a shared priority

Infrastructure investments are a shared responsibility, with the federal government generally partnering with other orders of government to invest in and deliver public infrastructure.

The public sector owns over two-thirds of infrastructure

- 71% of infrastructure in Canada is publicly owned, but the public share varies by asset.

Provinces, territories, and municipalities play critical roles

- 97% of infrastructure is owned by provinces, territories and municipalities.

Collaboration is key to delivering quality infrastructure

Although the federal government's share of owned infrastructure is growing, it mostly acts as a funder and supporter of projects.

The Government of Canada plays a major role in funding and administering infrastructure in Indigenous communities

The government is partnering with Indigenous communities to fulfill its commitment to close the infrastructure gap in Indigenous communities, which is critical to advancing reconciliation with Indigenous Peoples and fostering healthy, safe and prosperous Indigenous communities.

-

Figure 13 - Text version

Stock of Infrastructure, 2024 Asset Group Private Public Billions ($), current dollars Marine 7.347 9.597 Trains and Buses 10.645 12.946 Communication 1.291 47.532 Other 27.418 17.799 Water and wastewater 109.299 32.125 Transport 253.630 57.839 Institutional Buildings 323.812 47.883 Energy 204.156 183.471

Sources: Infrastructure Economic Account (Statistics Canada, released Mar 2025).

-

Figure 14 - Text version

Publicly-owned infrastructure by order of government, 2022 Ownership Net Stock (Percentage) Federal (14.7B) 3% Provincial, Territorial, Municipal ($411.7B) 97% Note: Net stock was used as a proxy for ownership. The Federal category includes Defense Services; Provincial/Territorial includes Hospitals, Nursing and residential care facilities, and Educational services. Other industries categories: Indigenous (Aboriginal) and Government Business Enterprises are excluded from this analysis.

Sources: Infrastructure Economic Account (Statistics Canada, released Mar 2025).

Infrastructure investments have almost doubled in the last two decades

After stagnating in the late 20th century, real annual investment in infrastructure has nearly doubled from 2003 to 2023.

- Public investment (+125%) has grown more than private investment (+96%). Endnote *

As the stock of infrastructure grows from increased investment, the level of depreciation to be addressed by sustained, ongoing investment also grows.

- In 2024, $133B was invested in infrastructure, surpassing depreciation by $32B. Endnote **

- Investment levels since 2000 have meant that the remaining useful life ratio of all assets in Canada has steadily increased from 51.5 to 59.6 – a significant improvement.Endnote ***

-

Figure 15 - Text version

Infrastructure Investment and Depreciation, Constant Dollars Year Public investment Private investment Total depreciation Billions ($) 1981 25.361 18.577 31.343 1983 23.459 15.298 32.838 1985 24.397 13.372 33.376 1987 24.671 12.937 33.912 1989 27.316 16.604 34.930 1991 30.067 17.874 36.617 1993 27.442 13.815 37.805 1995 28.086 12.791 38.295 1997 23.764 13.251 38.503 1999 24.689 17.281 38.645 2001 30.574 13.875 39.172 2003 34.430 13.715 40.182 2005 37.769 14.271 41.414 2007 44.044 17.479 43.581 2009 54.820 18.935 47.085 2011 55.905 24.844 51.846 2013 53.880 29.480 55.772 2015 55.520 30.274 59.681 2017 60.559 26.570 63.294 2019 59.816 28.293 66.921 2021 63.019 28.265 70.333 2023 67.941 29.216 73.437

Sources: Infrastructure Economic Account (Statistics Canada, released Mar 2025).

Understanding Infrastructure average age and remaining service life helps asset owners to inform early planning and management

- The average age and remaining useful service life of infrastructure assets have improved from a low point around 2000 and have remained stable since 2018.

- According to the Canadian Infrastructure Report Card, early investment in maintenance and repair, while an asset’s service life remains high, can eliminate or delay more costly rehabilitation or reconstruction spending in the future.

- Publicly sharing clear and relevant information on the status of infrastructure in Canada allows stakeholders and members of the public to gain insight on complex systems.

-

Figure 16 - Text version

Average Age and Remaining Useful Life Ratio of Total Infrastructure Assets Year Average age (Years) Remaining Useful Life (Ratio) 1981 12.1 61.8 1982 12.3 61.2 1983 12.6 60.5 1984 12.9 59.6 1985 13.1 58.7 1986 13.4 58 1987 13.7 57.2 1988 14 56.6 1989 14.1 56.1 1990 14.3 55.8 1991 14.4 55.6 1992 14.5 55.3 1993 14.6 54.8 1994 14.8 54.4 1995 14.9 53.9 1996 15.1 53.4 1997 15.3 52.8 1998 15.5 52.3 1999 15.6 51.9 2000 15.7 51.5 2001 15.8 51.4 2002 15.8 51.4 2003 15.8 51.5 2004 15.8 51.7 2005 15.7 52 2006 15.6 52.4 2007 15.4 52.9 2008 15.2 53.5 2009 15 54 2010 14.7 55 2011 14.4 55.8 2012 14.2 56.5 2013 14 57.1 2014 13.9 57.6 2015 13.8 58 2016 13.7 58.2 2017 13.3 59.3 2018 13.2 59.6 2019 13.1 59.6 2020 13.1 59.7 2021 13.1 59.6 2022 13.1 59.6 2023 13.1 59.6

Sources: Infrastructure Economic Account (Statistics Canada, March 2025 data)

The condition of infrastructure in Canada

More than half of Canada’s key road and water public infrastructure is in good or very good condition

However, condition varies among asset types and owners, and some assets have significant unknown conditions.

In 2022, the total replacement value of Canada’s core public infrastructure was estimated to be $2.3 trillion

More than half (62.5%) of Canada's assets by replacement value are in good and very good condition.

Approximately 16% of assets are in poor and very poor condition, accounting for $357 billion to replace.

Roads and water infrastructure accounted for over three-quarters of the total replacement value.

Rural municipalities owned most of the municipally owned roads (77.4% by length, excluding sidewalks), but they accounted for only 61.4% of the replacement value.

There is a significant infrastructure gap between Indigenous and non-Indigenous communities in Canada

E.g. estimated at $349.2 billion for First Nations communities and $75.1 billion in Inuit Nunangat.

-

Figure 17 - Text version

Key Road and Water Infrastructure Assets Condition, 2022 Asset Poor or Very Poor Fair Good or Very Good Unknown Road assets 15% 25% 52% 8% Non-linear portable water 8% 20% 65% 7% Linear Portable water 14% 20% 60% 6% Non-linear wastewater 12% 22% 60% 6% Linear wastewater 13% 20% 57% 11% Non-linear stormwater 6% 14% 54% 26% Linear stormwater 7% 20% 43% 30%

Sources: Canada’s Core Public Infrastructure Survey (CCPI), 2022 data (Statistics Canada, released October 2024). CCPI primarily samples units at the municipal level, with a census of municipalities with at least 1,000 residents, and a sample of rural municipalities with at least 500 residents.

-

Figure 18 - Text version

Replacement values according to the condition of assets and replacement values as a percentage of the total, 2022 Condition Replacement value Percentage Poor or Very Poor $356,687 16% Fair $254,176 11% Good or Very Good $1,437,432 63% Unknown $250,389 11%

Sources: Canada’s Core Public Infrastructure Survey (CCPI), 2022 data (Statistics Canada, released October 2024). CCPI primarily samples units at the municipal level, with a census of municipalities with at least 1,000 residents, and a sample of rural municipalities with at least 500 residents.

Asset management capacity is lower in smaller municipalities, and varies significantly among provinces and territories

In 2022, over half of local and regional government organizations in Canada had asset management plans in place for most of their core public infrastructure.

- Less than half of public sector organizations had asset management plans in 2022 for the following infrastructure: active transportation (33%); public transit (37%); and culture, recreation, and sport facilities (49%).

- In contrast, more than three-fifths had plans for roads (68%), potable water (64%), wastewater (64%), and bridges and tunnels (60%).

- A higher proportion of urban municipalities had asset management plans, compared with their rural counterparts. Solid waste infrastructure was the sole exception.

-

Figure 19 - Text version

A map of Canada depicts pie charts for each province and territory indicating the percentage of municipalities with asset management plans.

Percentage of municipalities with an asset management plan in 2022 Province Percent Asset Management Plan Percent No Asset Management Plan Alberta 85% 15% British Columbia 89% 11% Manitoba 70% 30% New Brunswick 97% 3% Newfoundland and Labrador 74% 26% Northwest Territories 51% 49% Nova Scotia 89% 11% Nunavut 16% 84% Ontario 99% 1% Prince Edward Island 89% 11% Québec 67% 33% Saskatchewan 90% 10% Yukon 88% 12% Canada 81% 19% Note: Ontario is the only jurisdiction with asset management planning legislation.

Sources: Canada's Core Public Infrastructure Survey (CCPI), 2022

Current and future infrastructure investments are influenced by key economic, socio-demographic and environmental factors

Canada's population is growing – faster than our G7 peers – increasing pressure on our existing infrastructure while generating additional need for new investments.

Macroeconomic headwinds coupled with elevated interest rates will contribute to higher borrowing costs. Fiscal constraints will require efficient allocation of funding to match real needs.

Extreme weather events are increasing, requiring renewed focus on disaster mitigation, adaption and climate change.

Cross-sectoral impacts of infrastructure - The economy

Beyond construction's immediate impact, infrastructure investment contributes to long-term economic competitiveness

The construction sector is essential to the Canadian economy - accounting for 7% of GDP - valued $152 billion. Households and businesses rely on quality infrastructure to facilitate the creation and transportation of goods, services and people that drive the long-term economic growth.

According to the IMF, in advanced economies, every $1 of public infrastructure investment can boost total economic output by $2.3 after 5 years.

The Global Infrastructure Hub (GIHub) estimates Canada's average infrastructure investment between 2016 and 2022 to be 2.5% of GDP - is 0.32 percentage points higher than the G7 average. However, more investment is needed to meet infrastructure demand – with the GIHub recommending additional annual investment of 0.04% of GDP.

-

Figure 20 - Text version

The Benefit of Public Infrastructure Investment Year Economic Output Generated for Each Dollar Invested Year 0 $0.00 Year 1 $0.80 Year 2 $1.30 Year 3 $1.70 Year 4 $2.10 Year 5 $2.30 Note: GDP growth over time for each dollar of public infrastructure investment.

Sources: International Monetary Fund (IMF) and Global Infrastructure Hub - A G20 INITIATIVE

-

Figure 21 - Text version

Canada invests more in infrastructure as a percentage of GDP than the G7 average Years Canada (investment) G7 countries, excluding Canada (investment) 2007 2.16% 2.04% 2008 2.33% 2.06% 2009 2.68% 2.11% 2010 3.07% 2.09% 2011 2.87% 2.06% 2012 2.69% 1.98% 2013 2.65% 1.96% 2014 2.58% 2.03% 2015 2.26% 1.95% 2016 2.49% 2.22% 2017 2.49% 2.21% 2018 2.52% 2.25% 2019 2.52% 2.23% 2020 2.5% 2.23% 2021 2.49% 2.22% 2022 2.49% 2.21%

Sources: International Monetary Fund (IMF) and Global Infrastructure Hub - A G20 INITIATIVE

A highly productive construction sector is critical to growing our infrastructure

A strong construction sector is needed to sustain Canada’s infrastructure

From connecting the country through advanced transit systems to providing roads, community buildings and wastewater facilities, Canadians rely on the construction sector to build essential and resilient infrastructure.

As the sector grapples with stagnant productivity, embracing innovative approaches and new technologies can enable the sector to meet growing demands.

Government transparency on the future of infrastructure will be necessary to foster industry confidence and incentivize the private sector's co-investment for sustained growth.

Key challenges facing the construction sector

- Labour shortages

- The construction sector is experiencing an extremely tight labour market with job vacancies exceeding unemployment rates.

- Retainment and recruitment are becoming increasingly difficult and meeting Canada’s construction labour force needs will require ongoing commitments to apprenticeship programs, training, and recruitment.

- By 2033, 21% of the current construction labour force is expected to retire, leaving the industry with a possible retirement-recruitment gap of 85,500 workers.

-

Figure 22 - Text version

Most of the labour shortages faced during the pandemic have normalized however the labour market remains tight Year Construction Vacancy Rate Construction Unemployment Rate Q4 2020 3.6% 7.6% Q1 2021 4.6% 9.8% Q2 2021 5.8% 5.7% Q3 2021 6.3% 4.0% Q4 2021 5.7% 4.6% Q1 2022 6.4% 7.4% Q2 2022 7.7% 4.7% Q3 2022 6.9% 2.9% Q4 2022 5.5% 3.9% Q1 2023 5.5% 7.6% Q2 2023 5.7% 5.3% Q3 2023 5.0% 3.7% Q4 2023 4.1% 4.7% Q1 2024 4.0% 7.8% Q2 2024 4.2% 5.5% Q3 2024 3.7% 4.3%

-

- Volatile commodity prices and supply chain concerns

- Volatile commodity prices and supply chain disruptions are forcing the construction sector to grapple with elevated project costs, project delays or abandonment.

Declining construction sector productivity risks limiting our ability to deliver Canada's infrastructure needs

Labour productivity in the construction sector has lagged other sectors in the past two decades

Between 2001 and 2023, productivity in the construction sector fell by roughly 10 percent from $54 per hour to $49 per hour, a two-decade low.

Low productivity in the construction sector can be attributed to several key factors including:

- Significant Fragmentation among firms

- Limited Investment in R&D

- High reliance on labour relative to capital

-

Figure 23 - Text version

Construction Sector Productivity Year Manufacturing All Industries Construction $ per hour (2017 chained) 1997 $47.9 $48.5 $50 2001 $56.5 $53.1 $53.1 2005 $60.3 $56 $55 2009 $60 $56.6 $52.1 2013 $65.5 $59.6 $54.5 2017 $68.1 $62.9 $54.4 2021 $69.6 $65.2 $54 Note: Manufacturing sector now produces 40% more than construction.

Sources: Table 36-10-0480-01 (Statistics Canada); Economic Analysis and Modelling, HICC

Poor construction sector productivity represents a drag on the overall canadian economy

The construction sector’s lagging productivity has limited its economic contribution, with an estimated $410-$538 billion (3 percent) in additional GDP that could have been generated over the past decade if productivity had kept up with other sectors.

-

Figure 24 - Text version

Construction Sector GDP Contribution Year Construction GDP Estimated GDP at Business Sector Productivity Growth Estimated GDP at Manufacturing Sector Productivity Growth Billions ($) 1999 84.91 91.39 92.58 2003 102.81 113.25 116.83 2007 125.28 135.11 141.08 2011 135.73 156.96 165.33 2015 153.25 178.82 189.58 2019 157.04 200.68 213.83 2023 164.95 222.54 238.08

Sources: Table 36-10-0480-01 (Statistics Canada); Economic Analysis and Modelling, HICC

Despite the number of residential construction workers doubling between 2001 and 2023, housing starts and completions grew by only 50 percent and 40 percent, respectively.

As a result, the number of workers needed to build 100 homes rose 45 percent from 49 in 2001 to 71 in 2023.

The construction sector is home to high paying jobs but the benefits are not equal across different working groups

Half of infrastructure jobs are concentrated in the construction industry

In 2023, infrastructure investment created 665,000 jobs (direct and indirect employment), of which 332,000 were in the construction sector. (Statistics Canada)

Among direct construction jobs, there were 58.2 million hours worked, with an average hourly wage of $35.5 (compared to a Canadian average of $33.6) in 2023.

Women had a lower average hourly wage than men - women earned on average $31.8 per hour, while men earned $36.1 per hour in 2023.

Since May 2015, the average wage for the unionized construction worker has increased by 20%, with particularly large increases in 2024.

There is untapped potential to diversify the construction labour force

The inclusion of certain groups to the labour force can help alleviate labour shortages and improve gender and visible minority participation; while ensuring that construction wages are distributed proportionally amongst Canadians.

-

Figure 25 - Text version

There is Untapped Potential to Diversify the Construction Labour Force

Non-Visible Minorities vs. Visible Minority

- Non-Visible Minorities: 89%

- Visible Minority: 11%

Men vs. Women

- Men: 88%

- Women: 12%

Newcomers vs. Canadian-Born

- Newcomers: 19%

- Canadian-Born: 81%

Indigenous Peoples vs. Non-Indigenous

- Indigenous Peoples: 5%

- Non-Indigenous: 95%

Adults (aged 25 to 54) vs. Youth (under 25) vs. Over 55

- Adults (aged 25 to 54): 69%

- Youth (under 25): 11%

- Over 55: 20%

Sources: Infrastructure Economic Account; Table 14-10-0037-01; Table 14-10-0064-01 (Statistics Canada)

Construction materials are an integral part of infrastructure delivery and subject to volatility

Key commodities such as cement, steel, lumber and aluminum form the foundation of infrastructure projects

- Cement is used in the construction of public transit railways; it is essential for building water treatment plants and is a main ingredient in concrete for residential building foundations.

- Steel is utilized in the manufacturing of rail tracks and train stations. It is important for pipelines and pumping stations in water infrastructure as well as for structural frames in building and residential construction.

- Aluminum is used in the manufacturing of buses and subway cars, while being an important element in ensuring water infrastructure's resistance to corrosion.

- Lumber is used in residential construction for framing as well as exterior and interior finishes.

Prices of construction materials are largely set by global markets and international supply and demand

- Increased demand from large countries (e.g. China, U.S.) creates competition for resources and drives prices up.

- Supply chain bottlenecks caused by transportation disruptions can lead to price fluctuations.

- Extreme climate events (e.g. wildfires) can also have an impact on material availability and costs.

Commodity prices for construction materials are inherently volatile

- Factors contributing to volatility include:

- Changes in global economic conditions

- Geopolitical events and trade policies

- Fluctuations in supply and demand dynamics

- As such, volatile prices can force the construction sector to grapple with elevated project costs, project delays or abandonment.

-

Figure 26 - Text version

Prices of Key Construction Commodities Year Lumber (USD/1,000 board feet) Aluminum (USD/T) Cement Price Index (Jan 2000 = 100) Hot-Rolled Coil Steel (USD/T) 2009 181 1,673 137.0 484.6926 2010 245 2,175 129.3 610.7333 2011 251 2,401 124.8 733.1884 2012 287 2,021 126.0 657.0502 2013 346 1,846 131.9 630.6667 2014 337 1,871 138.3 652.8996 2015 269 1,681 149.2 460.408 2016 300 1,611 156.5 520.9044 2017 385 1,970 163.2 619.5061 2018 461 2,111 167.0 828.6638 2019 371 1,800 171.0 602.1555 2020 519 1,724 172.8 576.0351 2021 882 2,482 179.6 1591.153 2022 787 2,711 197.1 1005.668 2023 510 2,347 218.8 964.9338

Sources: Trading Economics, FRED Economic Data.

Cross-sectoral impacts of infrastructure - The environment

Infrastructure is crucial to mitigating and adapting to climate change

Infrastructure is highly affected by climate change – natural disasters are more frequent and severe

Resilient infrastructure can better withstand and protect communities from impacts of climate change.

Use of climate-resilient infrastructure offers much potential to reduce risk

Data, guidance, standards and codes can help inform how infrastructure is located, designed, built and operated – to adapt to a changing climate.

-

Figure 27 - Text version

Number of Natural Disasters in Canada by Decade Years Number of Disasters 1900-1909 19 1910-1919 29 1920-1929 37 1930-1939 38 1940-1949 35 1950-1959 42 1960-1969 60 1970-1979 102 1980-1989 121 1990-1999 161 2000-2009 187 2010-2019 171 2020-2022 9

Sources: Canadian Disasters Database (Public Safety Canada, 2023); Canada's Top Climate Change Risks (Council of Canadian Academies, 2019).

-

Figure 28 - Text version

Adaptation Potential

This figure demonstrates the proportion of damages by category that can be avoided through adaptation measures. Nearly 40% of geopolitical dynamics and fisheries damages can be avoided through adaptation. Over 40% of ecosystems damages can be avoided through adaptation. Nearly 60% of forestry and water damages can be avoided through adaptation. Approximately 70% of coastal communities, northern communities and agriculture and food damages can be avoided through adaptation. About 80% of human health and wellness, physical infrastructure and governance and capacity damages can be avoided through adaptation.

Sources: Canadian Disasters Database (Public Safety Canada, 2023); Canada's Top Climate Change Risks (Council of Canadian Academies, 2019).

Infrastructure is highly impacted by climate change

Canada's infrastructure assets will fail earlier, require more investment in annual O&M, and will cost more to retrofit and replace due to changes in extreme heat and extreme precipitation.

| Province | Population | USL (Years) | O&M (% of CRV) | Renewal Cost (% added to CRV) | Retrofit Cost (% of CRV) | ||||

|---|---|---|---|---|---|---|---|---|---|

| Baseline | High emissions | Baseline | High emissions | Baseline | High emissions | Baseline | High emissions | ||

| BC | 5,448,894 | 62 | 35 | 1.5% | 4.2% | 0% | 31% | 0% | 34% |

| AB | 4,695,290 | 62 | 38 | 1.5% | 3.8% | 0% | 28% | 0% | 30% |

| SK | 1,167,711 | 62 | 46 | 1.5% | 3.0% | 0% | 21% | 0% | 22% |

| MB | 1,397,017 | 62 | 46 | 1.5% | 2.9% | 0% | 20% | 0% | 22% |

| ON | 15,608,369 | 62 | 47 | 1.5% | 2.9% | 0% | 19% | 0% | 20% |

| NB | 834,691 | 62 | 35 | 1.5% | 4.1% | 0% | 31% | 0% | 34% |

| PE | 173,787 | 62 | 15 | 1.5% | 6.3% | 0% | 53% | 0% | 58% |

| NS | 1,058,694 | 62 | 15 | 1.5% | 6.3% | 0% | 53% | 0% | 58% |

| NL | 538,605 | 62 | 17 | 1.5% | 6.1% | 0% | 50% | 0% | 55% |

| Canada | 30,923,058 | 62 | 41 | 1.5% | 3.5% | 0% | 25% | 0% | 27% |

| Note: Estimates based on comparing 1971-2000 baseline to 2071-2100 period. Analysis excludes territories and QC as analysis is ongoing. | |||||||||

Sources: FAO, Climatedata.ca, EAM calculations, Statistics Canada

-

Figure 30 - Text version

Arterial road assets in Toronto are estimated to fail 14 years earlier in the high emissions scenario by the end of the century compared to the baseline Age Baseline Low emissions – 2071-2100 Medium emissions – 2071-2100 High emissions – 2071-2100 Failure Threshold Repair target 0 1 1 1 1 0.35 0.8 10 0.89782 0.86681 0.85299 0.81953 0.35 0.8 20 0.67028 0.56133 0.51648 0.41979 0.35 0.8 30 0.37386 0.24715 0.20794 0.14348 0.35 0.8 40 0.17315 0.10449 0.08868 0.0678 0.35 0.8 50 0.08955 0.06334 0.05856 0.05317 0.35 0.8 60 0.06193 0.05316 0.05185 0.05056 0.35 0.8

Sources: FAO, Climatedata.ca, EAM calculations, Statistics Canada

-

Figure 31 - Text version

This figure demonstrates the estimated climate impact of Saskatchewan’s $5.5 billion portfolio of road assets based on different indicators: useful service life, operations and maintenance (O&M) costs, renewal costs, and retrofit costs. Useful service life could decrease by 17 years, from 62 years (stable climate) to 45 years (considering future climate conditions). Annual O&M costs could increase by $83 million annually, from $83 million (stable climate) to $166 million (considering future climate conditions). For renewal costs, $6.67 billion would be needed to replace existing stock with adapted assets, representing 21% in additional cost due to climate change (core replacement value at stable climate). For retrofit costs, $1.1 billion would be needed to retrofit all existing assets, representing 22% in retrofit costs due to climate change (core replacement value at stable climate).

Estimates based on comparing 1971-2000 baseline to 2071-2100 high emissions scenario.

Sources: FAO, Climatedata.ca, EAM calculations, Statistics Canada.

Resilient infrastructure requires efficient designs and planning

In 2023, transportation and buildings account for approximately 34% of all greenhouse gas emissions

What is built defines the range of options available to individuals and companies (e.g., transit vs. roads).

How infrastructure is built defines the baseline emissions level, as inefficient designs become "locked in". More efficient future designs are expected to reduce the operational emissions intensity of infrastructure. Current estimates suggest that future efficient designs will reduce operation emissions to 50% from the current level of 89%.

Overall, the percent of municipal owners of infrastructure in Canada that consider climate change mitigation and adaptation in their decision-making process remains low, at less than half of owners for most asset categories.

-

Figure 32 - Text version

Megatonnes of CO2-equivalent emissions by source Year Transportation and Buildings Other Sources 1990 190.5 398.1 1991 185.2 396.8 1992 189.2 410 1993 195.7 406.1 1994 202.1 419.8 1995 205 434.1 1996 214 446.9 1997 215.7 460.7 1998 210.5 472 1999 218.5 476.1 2000 226.1 493.2 2001 222.9 487.3 2002 229.4 486.2 2003 239.8 494.4 2004 243 493.6 2005 241.6 490.6 2006 237.4 487.9 2007 248.2 499.9 2008 248.6 482.1 2009 245.9 443.7 2010 247 454.9 2011 250.4 460.9 2012 249.1 467.2 2013 252.8 470.3 2014 250.9 469.3 2015 247.9 475.1 2016 247.3 457.8 2017 253.1 459.1 2018 261.7 462.9 2019 263.5 460.3 2020 232.3 426.6 2021 237.3 433.2 2022 243.4 456.5 2023 239.3 454.7

Sources: Greenhouse Gas Emissions (Environment and Climate Change Canada, 2025); GHG Emissions from Building Construction (Green Construction Board, 2014); Canada's Core Public Infrastructure Survey (CCPI)

-

Figure 33 - Text version

Role of climate change adaptation or mitigation in decision-making process, 2022 Assets Factored in climate change Did not factor in climate change Stormwater 50% 50% Bridges and tunnels 48% 52% Wastewater 45% 55% Portable water 44% 56% Roads 42% 58% Public transit 37% 63% Solid waste 31% 69% Culture, recreation and sports facilities 30% 70% Active Transportation 20% 80%

Sources: Greenhouse Gas Emissions (Environment and Climate Change Canada, 2025); GHG Emissions from Building Construction (Green Construction Board, 2014); Canada's Core Public Infrastructure Survey (CCPI)

Environmental improvements are being made during the construction of infrastructure assets

As investment increases, so do the levels of GHG emissions

However, greenhouse gas emissions per value added to the Canadian economy has decreased since 2009, suggesting that environmental improvements are being made during the construction of these assets.

Since 2009, the proportion of infrastructure industries’ clean inputs have increased, reaching 3.2% in 2024. Environmental and clean technology inputs have increased from $1.66 billion in 2009 to $4.24 billion in 2024.

- The proportion of clean input assesses whether an infrastructure asset was constructed using environmental and clean technology inputs (a process/product/service that reduces environmental impacts).

-

Figure 34 - Text version

GHG and GHG per value added Year GHG (Tonnes) GHG per value added (Tonnes per thousand dollars) 2009 15,020 0.3035 2010 17,009 0.3045 2011 15,788 0.283 2012 15,510 0.2695 2013 15,109 0.2494 2014 14,588 0.2363 2015 15,200 0.242 2016 15,683 0.2524 2017 16,376 0.2485 2018 16,595 0.2417 2019 16,075 0.2345 2020 15,427 0.2128 2021 14,778 0.1895 2022 14,826 0.1704 2023 15,902 0.169 2024 16,452 0.1647

Sources: Infrastructure Economic Accounts (March, 2025)

-

Figure 35 - Text version

Clean Input Proportion Years Total Investment (Billions) Clean Input Proportion 2009 $62.803 2.7% 2010 $72.841 2.7% 2011 $72.654 2.7% 2012 $75.134 2.7% 2013 $78.300 2.8% 2014 $81.808 3.0% 2015 $84.061 3.2% 2016 $82.416 3.3% 2017 $87.129 3.0% 2018 $91.657 3.2% 2019 $92.761 3.2% 2020 $97.078 3.2% 2021 $104.793 3.3% 2022 $116.730 3.2% 2023 $126.137 3.2% 2024 $133.759 3.2%

Sources: Infrastructure Economic Accounts (March, 2025)

Cross-sectoral impacts of infrastructure - Our communities

Infrastructure impacts a community’s ability to participate in the economy and provides opportunities to underserved populations

Connectivity is an essential service and a prerequisite to participate in the digital economy:

- The CRTC’s target is to have 100% of homes and businesses have access to 50Mbps download and 10Mbps upload with unlimited data by 2031.

- While targets are on track, there is a large gap between First Nations communities and the rest of Canada.

- A gap remains between those households with access to ultra-fast speeds (Gigabit internet) and those without.

Strong communities requires easy access to social and health services, including high levels of proximity to public transportation in Canada's metropolitan areas:

- Canada's largest metropolitan areas have the most convenient proximity to public transportation at over 80% of the population within 500 m of public transit.

- Convenient access to public transport is generally lower in smaller metropolitan areas.

-

Figure 36 - Text version

Broadband Service Availability Year 50/10/Unlimited Gigabit 50/10/Unlimited First Nations Gigabit First Nations 2018 86% 65% 31% 23% 2019 87% 61% 35% 22% 2020 90% 76% 39% 31% 2021 91% 77% 43% 32% 2022 93% 83% 51% 38% 2023 95% 89% 59% 43%

Sources: CRTC Communications Monitoring Report (Accessed April 2025); Statistics Canada Table 23-10-0313-01 Access to public transport by distance and public transport carrying capacity, geography, gender, and selected demographic and socio-economic characteristics

-

Figure 37 - Text version

Percentage of population less than 500 m from public transit stop City Percentage of population within 500 metres of a public transit stop Regina 87% Montréal 86% Victoria 85% Vancouver 84% Toronto 84% Winnipeg 83% Québec 80% Calgary 79% Kitchener - Cambridge - Waterloo 75% Edmonton 74% Hamilton 72% London 70% Halifax 66% Moncton 63% St John's 55%

Sources: CRTC Communications Monitoring Report (Accessed April 2025); Statistics Canada Table 23-10-0313-01 Access to public transport by distance and public transport carrying capacity, geography, gender, and selected demographic and socio-economic characteristics

The state of infrastructure – A summary

- Canada’s infrastructure stock has grown to over a trillion dollars over the last decade. Ongoing investment is needed to offset the effects of depreciation.

- HICC has continued to fund the renewal and expansion of public transit in Canada to great success. However, since 2021, HICC has made significantly less contributions to traditional core infrastructure assets like highways, roads, and drinking water or wastewater assets. Condition data in these areas reflect the declining state of roads and linear water assets.

- The expansion and alignment of economic-enabling infrastructure funding into roads, highways, and shortline rail can support resilience in the economy and renew existing infrastructure.

- Existing infrastructure is vulnerable to the increasing frequency and intensity of natural hazards. Maintaining a presence in funding resilience is critical to the long-term viability of Canadian infrastructure.

- Continuing to generate infrastructure data is crucial for accurately assessing the economic importance of infrastructure spending in Canada, as it enables evidence-based decision-making, helps measure long-term impacts on productivity, growth, and quality of life, and ensures accountability in public investment.

Section C: State of Transit

Does Canada have the right kind of transit infrastructure to meet current and future needs?

- To answer this question, we need to understand both the state of our transit infrastructure and how it interacts with the surrounding housing, land-use, and other factors that affect the choices people make about getting around their communities.

- Canada’s current state of transit infrastructure can be assessed according to:

- Stock: Accumulation of an inventory of tangible transit assets over time.

- Investment: Transit spending for the purposes of construction of tangible assets.

- Condition: Standardized scale used to define the current state of an asset (i.e., very good, good, fair, poor, or very poor).

- To understand other factors, we can consider factors such as access to transit and whether people live in transit- and active transportation-friendly communities or in more car-oriented areas.

Why is it important to invest in public transit and what is HICC's role?

- Investments in transit infrastructure provide direct and indirect economic benefits, including job creation linked to project design and construction, and additional economic activity that comes with greater mobility of people and goods once new infrastructure is in use.

- Access to transit and active transportation (cycling, walking) is an essential service across the country that can provide efficient and cost-effective transportation for people to access jobs and amenities like education, health care, and groceries. It also reduces traffic congestion and air pollution and saves on household costs.

- Local transportation is primarily a provincial, territorial, and municipal responsibility. Housing and other land-use decisions determine how far people need to travel from home to get to work, school, and other destinations, and what transportation modes they have available.

- More than four million people live in rural areas, where a lack of transit and safe mobility options disproportionally impact Indigenous Peoples, persons with disabilities, and the elderly.

Historically, public transit has been HICC’s largest area of investment, reflecting a high level of demand for investment across the country.

-

Figure 38 - Text version

Transit as a Share of Departmental Spending

- Public Transit and Active Transportation: 49%

- Transportation: 17%

- Green Infrastructure: 15%

- Sports and Recreation: 4%

- Drinking Water: 5%

- Culture and Tourism: 3%

- Other: 7%

The Department funds the planning, construction, and procurement of public transit and active transportation infrastructure, ties funding to requirements to ensure investments are made under the right enabling conditions and to support housing objectives and works to support and engage with the sector through research, data, and partnerships. Given the scale of HICC investments in public transit over time, this support has now been situated within a standalone, permanent program.

The Canada Public Transit Fund provides permanent funding to address a range of transit needs

- Launched in July 2024, the Canada Public Transit Fund is Canada’s first permanent public transit funding – providing an average of $3 billion annually.

- Three overarching streams support communities of all sizes, with funding flowing beginning in 2026-27. This design also recognizes that a place-based approach works better to support rural transit, where fixed routes are not always the best solution.

- Designed with extensive engagement from stakeholders across the country.

Baseline Funding

Baseline Funding will provide predictable, long-term funding to communities with existing transit systems to support routine investments, with an expected focus on public transit and active transportation system expansions, improvements, and state of good repair.

Metro-Region Agreements

Metro-Region Agreements will support the long-term development of public transit infrastructure in large urban areas. Through these agreements, the federal government will allocate funding and work with our partners to support the planning and construction of a broad range of projects, including major expansion.

Targeted Funding

Targeted Funding will provide flexible, call-specific funding to address federal priorities that meet local needs. Funding will cover areas such as rural transit, active transportation and zero emission solutions.

The Canada Public Transit Fund builds on the $33 billion Investing in Canada Infrastructure Program, which will continue to flow funds to approved transit projects into the 2030s through its Public Transit Infrastructure and Green Infrastructure streams.

Current stock, investment and condition of transit infrastructure

Growing investment in a shared priority

- Total annual capital spending in the transit sector rose by 194%, from $5.59 billion to $10.84 billion, between 2014 and 2023. Endnote *

- Provinces and territories accounted for most capital spending in that period, averaging 59.3% annually, followed by municipalities at 27.7%, and the Government of Canada at 13%. Endnote **

- Based on replacement value, in 2022 local and regional governments owned 76% of public transit assets and 82% of active transportation infrastructure. Endnote ***

- This growing investment has helped increase the stock and improve the condition of transit assets for many systems across Canada.

-

Figure 39 - Text version

Annual capital spending in the transit sector Years Federal Capital Contribution Provincial Capital Contribution Municipal Capital Contribution Other Capital Contribution 2010 18% 58% 21% 3% 2011 13% 69% 15% 3% 2012 12% 67% 17% 4% 2013 14% 2.7% 2.7% 2.7% 2014 12% 63% 19% 6% 2015 14% 63% 17% 6% 2016 15% 65% 16% 5% 2017 13% 61% 25% 2% 2018 15% 64% 20% 1% 2019 18% 58% 22% 2% 2020 13% 67% 19% 1% 2021 9% 73% 17% 1% 2022 10% 72% 18% 1% 2023 9% 73% 16% 2%

-

Figure 40 - Text version

Figure 1

- Local and regional: 76%

- Provincial and territorial: 24%

- Federal: 0%

Figure 2

- Urban munis over 200k: 76.2%

- Urban munis under 200k: 4.4%

- Regional orgs.: 19.2%

Source: Canada's Core Public Infrastructure Survey, 2022. Data for provincial and territorial active transportation replacement value and regional organizations for transit and active transportation is imputed.

-

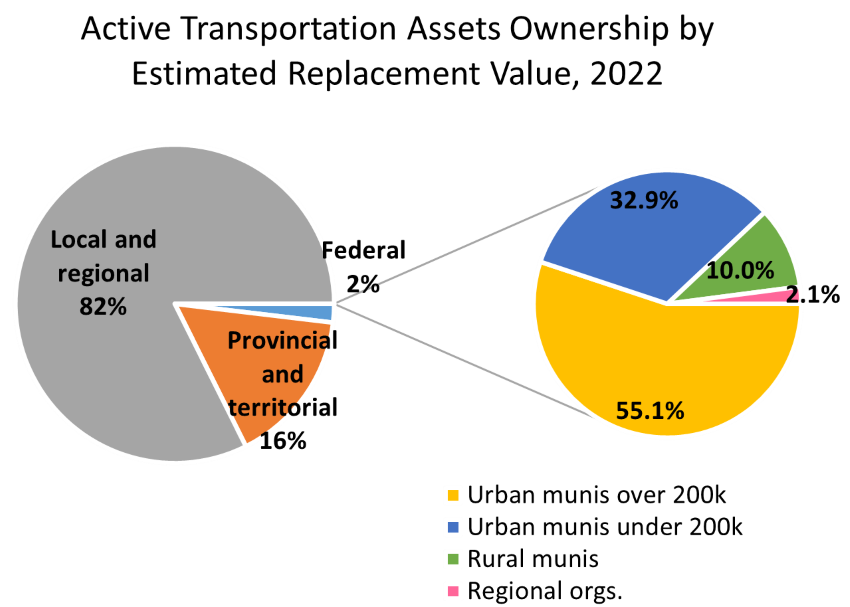

Figure 41 - Text version

Figure 1

- Local and regional: 82%

- Provincial and territorial: 16%

- Federal: 2%

Figure 2

- Urban munis over 200k: 55.1%

- Urban munis under 200k: 32.9%

- Rural munis: 10.0%

- Regional orgs.: 2.1%

Source: Canada's Core Public Infrastructure Survey, 2022. Data for provincial and territorial active transportation replacement value and regional organizations for transit and active transportation is imputed.

Stock of transit infrastructure

Public transit infrastructure includes fixed assets and rolling stock. In 2022Endnote *, we had:

- Over 7,100 single-track km of roads and over 1,500 km of rail, including 167 dedicated right-of-way bus lanes.

- Over 1,000 passenger stations and terminals, and over 30,000 transit shelters.

- Rolling stock of about 18,300 buses and 2,250 heavy rail vehicles (or subway railcars), and 376 light railcars.

-

Figure 42 - Text version

Public Transit Assets by Estimated Replacement Value, 2022 Assets Estimated Replacement Value (Billions, 2022 Dollars) Buses 17.4 Railcars 18.2 Other rolling stock assets 4.4 Passenger stations and shelters 15.6 Maintenance, storage and other facilities 17.3 Transit-exclusive bridges 7.3 Transit-exclusive tunnels 22.2 Transit-exclusive tracks and roads 9.7

Source: Statistics Canada, Inventory of core public infrastructure assets

-

Figure 43 - Text version

Active Transportation Assets by Estimated Replacement Value, 2022 Assets Estimated Replacement Value (Millions, 2022 Dollars) Bikeways or cycleways 6.5 Footbridges 3.7 Paved pathways 4.7 Trails (non-paved) 2.7 Sidewalks 44.2 Pedestrian tunnels 0.8

Source: Statistics Canada, Inventory of core public infrastructure assets

Active transportation infrastructure includes sidewalks, bike lanes and parking, bikeshare stations, bikes and e-bikes.

In 2022, we had nearly 146,000 km of sidewalks across Canada and two-thirds of neighbourhoods had cycling infrastructure.

Condition of transit infrastructure (general)

- Public transit assets and active transportation had an estimated replacement value of almost $175 billion at the end of 2022Endnote *. Many transit systems anticipate significant upgrades to maintain service and meet modern standards.

- A sample of ten of the largest public transit agencies shows a combined required state of good repair spending target of approximately $20.6B (2023 to 2032).

Where asset condition is known:

- Transit-exclusive tracks and roads are mostly in fair, good, or very good condition.

- Most buses, railcars, and other “rolling stock” are good or very good condition, especially electric buses and hybrid vehicles.

- 17% of public transit assets and 42% of active transportation assets – $45.7B in replacement value – are in unknown physical condition.

Fixed transit assets are generally in good condition, but a sizeable amount of some asset classes are in unknown condition (percentage)

-

Figure 44 - Text version

Estimated replacement value of core infrastructure assets, by physical condition Infrastructure assets Very Poor Poor Fair Good Very Good Unknown Total Public Transit 3% 10% 15% 28% 27% 17% Transit-exclusive network and roads 0% 4% 14% 25% 12% 45% Transit-exclusive bridges 0% 7% 20% 40% 34% 0% Maintenance and storage facilities 5% 8% 11% 30% 20% 26% Transit shelters 0% 3% 10% 31% 23% 33% Passenger stations/terminals 2% 6% 14% 35% 16% 27% Other rolling stock assets 2% 1% 12% 11% 37% 37% Buses 5% 12% 21% 30% 25% 7%

Note: This shows the physical condition rating of public transit assets, not including rolling stock. Bridges and tunnels are those exclusively used for public transit. This data is from Statistics Canada’s CCPI (2022). Table: 34-10-0284-01 (2024-10-21) Estimated replacement value of core public infrastructure assets, by physical condition rating

Current Outcomes

Transit is inherently linked to housing: More housing near transit means more riders

- Transit-oriented development, or TOD, is an approach to urban development that concentrates housing, businesses, and services near transit.

- It increases access to transit, meaning more riders and makes transit more economical.

- It enables the creation of more housing through density, which supports affordability.

- Although high-capacity transit, such as subway or light rail lines, offers the greatest opportunities for TOD, extensive urban bus networks are also key to enabling higher-density development.

- 81% of urban dwellers overall live within 500 metres of a public transit station or stop.

- 98% of urban dwellers living in a five-storey or higher apartment building were within 500 metres.

- Transit-oriented development is therefore a key tool for tackling Canada’s housing supply and affordability challenges, especially as networks continue to expand.

-

Figure 45 - Text version

% Residents of Different Housing Types within 500M of transit Housing Types Percentage within 500 metres of transit Single Family Home 73% Row House 86% 5 Storey-Plus 98%

Source: Statistics Canada, How far to the nearest transit stop?

| Region | Average Population Density (Census Subdivision) | Density within 800M of Transit Station |

|---|---|---|

| Vancouver City | 5,750 | 6,482 |

| Toronto City | 4,428 | 8,246 |

| Montréal Ville | 4,833 | 6,756 |

Source: Statistics Canada: General Transit Specification Feed, Census 2021, Census of Population 2021, Dissemination Block Boundary File; HICC calculations.

Land-use patterns combine with other factors to favour car travel, though people had increasingly been shifting to transit

- Even in Canada’s largest urban centres, most people live in suburbs or exurbs outside the city core with a high per-rider cost to operate transit.

- This results in high costs from car ownership, congestion, emissions, and more.

- In the fourth quarter of 2024, households spent over $56.3 billion to purchase, park, maintain, fuel, and insure personal vehicles (compared to $1.3 billion on urban transit).

- This development pattern poses challenges for increasing transit and active transportation use, though it is possible with sustained investment.

- Driven by urbanization and these types of costs, the share of commuters using public transit or active transportation was growing steadily prior to the COVID 19 pandemic.

-

Figure 47 - Text version

Vancouver

- Active Core: 16%

- Transit Suburb: 15%

- Auto Suburb: 67%

- Exurban: 2%

Toronto

- Active Core: 12%

- Transit Suburb: 15%

- Auto Suburb: 70%

- Exurban: 3%

Montréal

- Active Core: 17%

- Transit Suburb: 13%

- Auto Suburb: 67%

- Exurban: 3%

Edmonton

- Active Core: 7%

- Transit Suburb: 12%

- Auto Suburb: 72%

- Exurban: 9%

Calgary

- Active Core: 12%

- Transit Suburb: 8%

- Auto Suburb: 77%

- Exurban: 3%

Ottawa – Gat.

- Active Core: 14%

- Transit Suburb: 9%

- Auto Suburb: 62%

- Exurban: 15%

Source: Canadian Suburbs Atlas; 2021 Census, Statistics Canada.

| Year | Car/truck/van | Public Transit | Active Transportation | Other |

|---|---|---|---|---|

| 2024 Endnote * | 81.5% | 11.4% | 6.0% | 1.1% |

| 2021 Endnote * | 84% | 7.8% | 6.1% | 2.1% |

| 2016 Endnote * | 79.4% | 12.6% | 6.8% | 1.2% |

| 2011 Endnote ** | 79.7% | 12% | 7% | 1.2% |

Post-covid recovery and high costs are key challenges today

- Transit ridership and revenue collapsed during the COVID-19 pandemic and have been slow to recover—since then, transit agencies of all sizes have struggled with operational shortfalls.

- In 2019 fare revenues covered 51% of all transit operations costs, compared to 32% in 2022.

- Canada’s January 2025 data shows ridership was up from the previous year, but still 82.2% of January 2019; operating revenue was about 90.7% of January 2019.

-

Figure 49 - Text version

Canadian Transit Ridership (Jan 2019 - Jan 2025) Year Revenue (Millions of Dollars) Ridership (Millions of Passenger Trips) Pre-COVID Revenue Average Pre-COVID Ridership Average 2019 349.8 160.9 347.34 158.1 2020 365.9 163.9 347.34 158.1 2021 114.8 46.4 347.34 158.1 2022 160.5 64.8 347.34 158.1 2023 265.4 113.6 347.34 158.1 2024 298 124 347.34 158.1 2025 321.7 130.7 347.34 158.1

Source: Statistics Canada Monthly Ridership Data.

- Canada is one of the costliest countries in the world when it comes to building transit. A 2024 reportEndnote * ranked Canada 9th highest out of 60 countries for average cost-per-kilometre of new transit.

- Both hard cost (e.g., overbuilding, construction methods, customizations) and soft cost (e.g., reliance on private sector consultants, high contingency budgets) play a role.

-

Figure 50 - Text version

In a series of six graphs, two graphs demonstrate a relatively steady cost of construction for transit projects in Canada and the Anglosphere, with costs between $250M and $500M per KM between 2000 and 2020, with rapid projected increases to $1.25M per KM after 2030. The other four graphs depict relatively stable costs in countries with low costs for transit construction: Italy, Spain, South Korea, and Turkey, where costs typically remain between $250M and $500M per KM from 2000 to 2030.

Source: Aevaz, R. et al. 2022; Goldwyn, E et al. 2023; Wickens, S. 2020.

Future infrastructure needs

Canada’s growing population will sustain demand

- Statistics Canada expects Canada’s population to grow from 39.3 million in 2023 to 45.35 million in 2030, which HICC expects to mean an increase from 15.74 million commuters to 17.61 million.

- Larger urban areas are growing faster than Canada as a whole (15.3% since 2014) with small cities (9%) and rural communities (6.5%) seeing modest growth.

- This will likely mean more ridership, as the higher housing density in urban areas is associated with higher transit use.

- Transit agencies are anticipating some $150B in spending on network expansion over the next decade; other methods of estimation also show high expected spending.

-

Figure 51 - Text version

Large capital investment plans reflect transit agencies bracing for high congestion and urban population growth Years Historic Capital Expenditures Mid Scenario Demand Analysis Mid Commuter Growth Sustainable Targets Analysis Capital Investment Plans Implied Trend Annual Capital Investment, Billions ($) 2011 4.753 - - - 2015 7.253 - - - 2019 8.567 - - - 2023 - 10.545 10.735 12.001 2027 - 11.928 11.839 13.891 2031 - 13.545 13.171 16.082 2035 - - - -

| Need Scenario | Montréal | Vancouver | Toronto | Rest of Canada | Total |

|---|---|---|---|---|---|

| 10-year historic capital expenditure (2013-2023) | 11.1 | 3.4 | 50.1 | 14.9 | 79.5 |

| (1) Demographic, Social and Housing Density Demand (2025-2034) | 16.6 | 8.2 | 74.7 | 30.2 | 129.8 |

| (2) Target 22% sustainable commute share (2025-2034) | 18.6 | 8.4 | 70.3 | 29.8 | 127.1 |

| (3) Stated Capital Investment Plans (2025-2034) | 19.6 | 11.4 | 94.8* | 27.3 | 153.1 |

Note: Investment plans include 12 transit agencies representing > 95% of historic investment. |

|||||

Growing transportation emissions point to continued need for investment in sustainable modes such as transit

Passenger modal shift is essential for achieving climate targets require continued investment in transit and active transportation.

- Transportation is projected to be Canada’s largest emissions source in 2030.

- Electrification is not moving fast enough to meet near-term climate targets alone.

- Modal shift remains central: vehicle kilometres travelled (VKTs) drive emissions, and mode shift means fewer VKTs.

Emissions can be further reduced through transit electrification.

- ~500 ZEBs are currently on the roads, with thousands more funded or on order as the industry continues to transition.

- Canadian bus manufacturers are expanding domestic production of ZEBs, but the industry continues to face supply chain concerns and delays.

-

Figure 53 - Text version

Embodied CO2 emissions, per resident, by built environment Built Environment Kilograms, CO2e Montréal Row Houses 5,500 Montréal High Rises 15,500 Montréal Suburban 26,500 Toronto Row Houses 13,000 Toronto High Rises 16,000 Toronto Suburban 26,000 Rural 130,000

Source: Canadian Suburbs Atlas; 2021 Census, Statistics Canada.

-

Figure 54 - Text version

Proportion of population by neighbourhood type, all census metropolitan areas, 2021

- Compact Core: 13.6%

- Transit-Oriented Suburb: 11.1%

- Car-Dependent Suburb: 67.3%

- Exurb: 8.0%

Source: Canadian Suburbs Atlas; 2021 Census, Statistics Canada.

-

Figure 55 - Text version

Zero-emission Transit Buses Funded, Procured, and in Operation, as of July 2024 State of Zero-emission Transit Buses Percentage Received Funding 7.3% In Procurement 4.1% Battery Electric (In service) 1.6% Trolley (In service) 1.5%

-

Figure 56 - Text version

Population using public transit or active transportation for commuting Year Percentage 2016 19.4 (Starting value) 2021 13.9 2022 14.8 2023 16.1 2024 17.4 2025 18.2 2026 18.9 2027 19.7 2028 20.5 2029 21.2 2030 22.0 (Target value)

The state of transit – summary

- Public transit and active transportation infrastructure are critical to urban mobility, affordability, and prosperity and inherently linked to housing.

- Canada’s transit networks have grown substantially and are in a good state of repair following a decade of sustained investment, though agencies continue to face revenue challenges and financial pressures on operations post-COVID-19.

- Need for federal funding remains strong, as transit agencies plan significant investments in expansion and in maintaining good repair of recently expanded networks over the next decade, underpinned by population growth, urbanization, and concerns around congestion and emissions.

- HICC has established a solid and flexible base to support transit investments, helping to meet demand and achieve broader objectives related to housing, climate change, and access for transit-dependent populations.

- There are opportunities for collaboration among levels of government, stakeholders, and partners to improve mobility outcomes across Canada and ensure value for money of planned investments.

Annex: Regional Lens

Major rail transit investments are planned or underway across Canada

-

Figure 57 - Text version

- Greater Vancouver Area

- Surrey Langley SkyTrain

- Millennium Line Broadway Extension

- Expo and Millennium Upgrade Program

- Calgary

- Calgary Green Line

- Edmonton

- Valley Line LRT

- Capital Line South Extension

- Greater Toronto/Hamilton Area (Outside Toronto)

- Hazel McCallion LRT Extension in Brampton

- GO Transit Expansion

- Hamilton Light Rail Transit

- Toronto (City)

- Ontario Line

- Scarborough Subway Ext.

- [redacted]

- Eglinton Crosstown West Ext.

- Finch West LRT

- Ottawa

- Ottawa LRT Stage 2

- Greater Montreal Area